QQ登錄

QQ登錄 微博登錄

微博登錄 微信登錄

微信登錄

財(cái)務(wù)報(bào)告與分析中章節(jié)的設(shè)置是循序漸進(jìn)、逐層深入的,前面介紹的術(shù)語在后面還會(huì)有詳細(xì)的解釋與探討。

由于財(cái)務(wù)報(bào)告與分析本身自立體系,它是上市公司和報(bào)表使用人之間溝通交流的語言,所以學(xué)起來與外語學(xué)習(xí)有幾分相似。

財(cái)務(wù)報(bào)告與分析一共分為四大部分:

第一部分是掃盲階段,主要介紹財(cái)務(wù)術(shù)語、體系等基本知識(shí)。

在此基礎(chǔ)上,第二部分更深入地講解財(cái)務(wù)報(bào)表編制以及財(cái)務(wù)報(bào)表分析的方法。

進(jìn)一步地,第三部分針對(duì)存在利潤操縱空間的重點(diǎn)科目做詳細(xì)、深入的討論。

最后,第四部分是前面三部分內(nèi)容的綜合應(yīng)用。

四大部分在考試中占比最大的是第二部分和第三部分,大概占財(cái)報(bào)分析所有題目的80%以上。其次是第一部分,占比10%左右。

由于第四部分是財(cái)務(wù)分析的綜合應(yīng)用,不太適合一級(jí)的出題形式,所以出題比例相對(duì)比較少,大概占5%左右。

Questions 1:

A company operating in a highly fragmented and competitive industry reported an increase in return on equity(ROE)over the prior year.Which of the following reasons for the increase in ROE is least likely to be sustainable?The company:

A、increased the prices of its product significantly.

B、decided to make greater use of long-term borrowing capacity.

C、implemented a new IT system,allowing it to reduce working capital levels as a percentage of assets.

【Answer to question 1】A

【analysis】

A is correct.

An increase in price is not sustainable in a fragmented and competitive industry.Fragmented industries tend to be highly price competitive because of the need to increase market share and undercut prices in an attempt to steal share.

B is incorrect.Increasing the use of long-term borrowing capacity will increase leverage and increase ROE and is sustainable as long as the company maintains that level of leverage.

C is incorrect.By lowering the amount of working capital in the business,the company lowered its average total assets and average shareholders’equity and increased its turnover ratio.Holding all else equal,a lower average total asset will increase the ROE through the higher turnover ratio.This strategy is sustainable because it relies on an improvement in productivity generated by new technology(new IT system).

Questions 2:

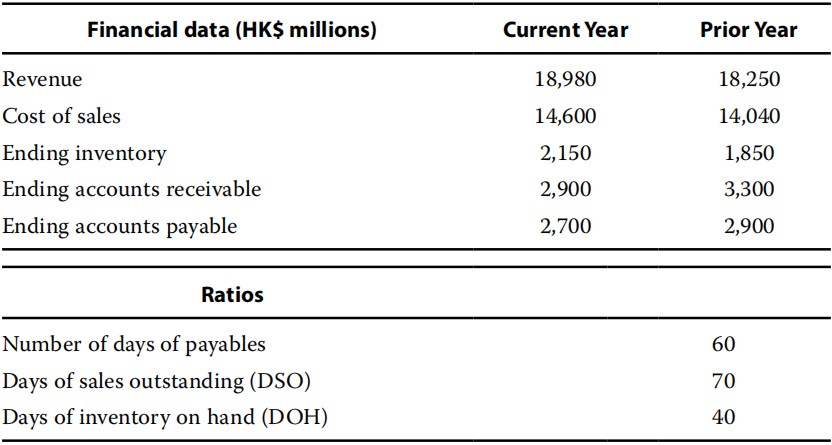

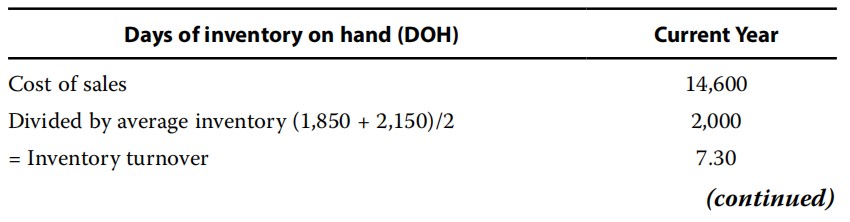

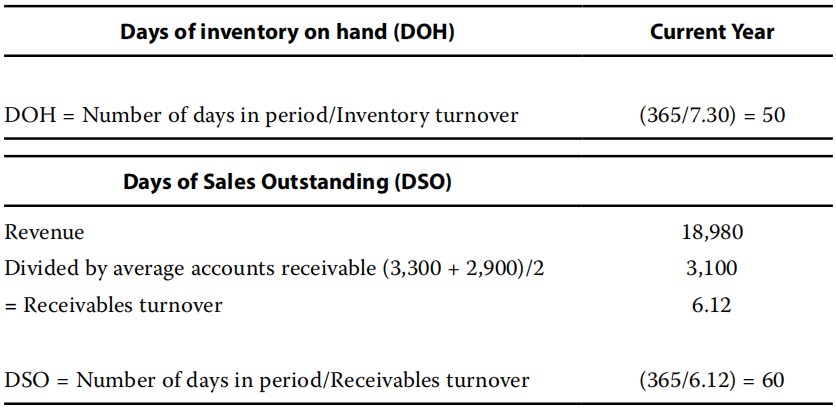

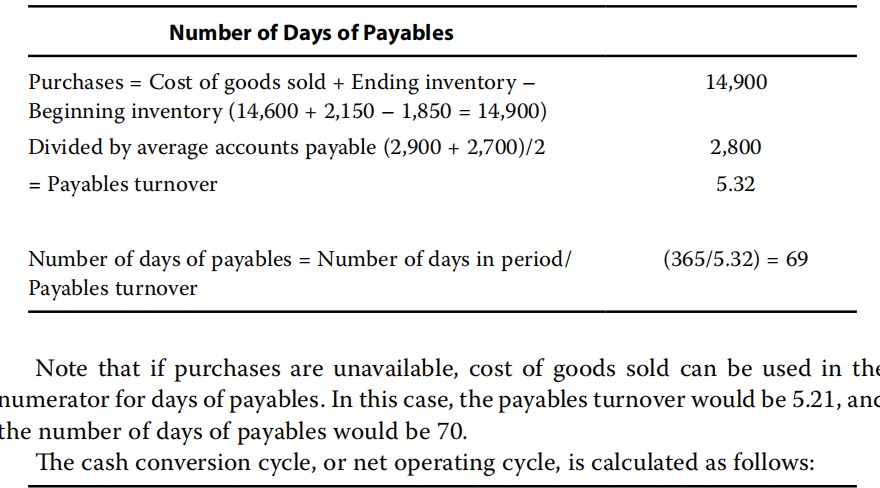

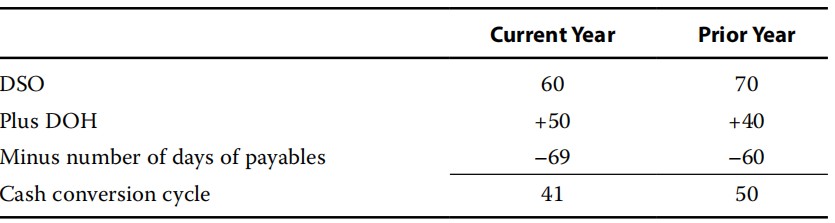

The following data are available on a company:

The least likely explanation for the improvement in the cash conversion cycle is that the firm improved on its:

A、ability to collect from customers.

B、payments to suppliers.

C、inventory management.

【Answer to question 2】C

【analysis】

C is correct.The cash conversion cycle=DSO+DOH–Days in payables

The company’s cash conversion cycle improved.The reduction in days of sales outstanding indicates that the company improved its collections from customers and shortened the cash conversion cycle.The increase in number of days of payables indicates that the company took longer to pay suppliers,which also shortened the cash conversion cycle and indicates greater liquidity.The only metric that deteriorated is days of inventory on hand,which indicates that the company tied up more capital in inventory.Therefore,inventory management did not improve the cash conversion cycle.

A is incorrect.The reduction in days of sales outstanding indicates that the company improved its collections from customers.This also served to shorten the cash conversion cycle and indicates greater liquidity.Therefore,the response is valid as it did represent an improvement.

B is incorrect because the increase in number of days of payables indicates that the company took longer to pay suppliers,which served to shorten the cash conversion cycle and indicates greater liquidity.Therefore,the response is valid as it did represent an improvement.

相關(guān)閱讀

延伸閱讀

以上就是【CFA財(cái)務(wù)報(bào)表分析練習(xí)題"Financial Report":Financial Analysis】的全部內(nèi)容,如果你想學(xué)習(xí)更多CFA相關(guān)知識(shí),歡迎大家前往高頓教育官網(wǎng)CFA頻道!在這里,你可以學(xué)習(xí)更多精品課程,練習(xí)更多重點(diǎn)試題,了解更多最新考試動(dòng)態(tài)。